Financial reporting developments

A comprehensive guide

Impairment or

disposal of long-

lived assets

Revised December 2023

To our clients and other friends

ASC 360-10, Impairment and Disposal of Long-Lived Assets, provides accounting guidance for impairments

of assets that are held for use, held for sale and to be disposed of by other means. In one of its more

challenging aspects, ASC 360-10 requires the use of fair value measurements for impairment of assets

that are unique and not widely traded. The following publication provides an overview of the accounting

for asset impairments as well as interpretive guidance.

We hope this publication will help you understand the accounting for the impairment or disposal of long-

lived assets. We are available to assist you in understanding and complying with this standard and are

ready to answer your particular concerns and questions.

December 2023

Financial reporting developments Impairment or disposal of long-lived assets | i

Contents

1 Overview ................................................................................................................... 1

1.1 Introduction ........................................................................................................................... 1

1.2 Scope .................................................................................................................................... 2

1.3 Long-lived assets to be held and used ............................................................................. 5

1.3.1 Indicators of impairment — Step 1 ................................................................................... 5

1.3.2 Test for recoverability — Step 2 ....................................................................................... 5

1.3.3 Measurement of an impairment loss — Step 3 .................................................................. 6

1.3.4 Allocation of an impairment loss..................................................................................... 6

1.3.5 Reporting and disclosure of impairments ........................................................................ 6

1.4 Long-lived assets to be disposed of other than by sale .............................................................. 7

1.5 Long-lived assets to be disposed of by sale .............................................................................. 7

1.5.1 Held for sale criteria ...................................................................................................... 7

1.5.2 Measurement ................................................................................................................ 8

1.5.3 Grouping of assets held for sale ...................................................................................... 8

1.5.4 Changes to a plan of sale ............................................................................................... 8

2 Long-lived assets to be held and used .......................................................................... 9

2.1 Overview ............................................................................................................................... 9

2.2 Indicators of impairment — Step 1 ......................................................................................... 10

2.2.1 Depreciation estimates ................................................................................................ 11

2.3 Test for recoverability—Step 2 ............................................................................................... 12

2.3.1 Grouping long-lived assets to be held and used .............................................................. 12

2.3.1.1 Debt in asset groups.................................................................................. 14

2.3.1.2 Impairment indicators for individual assets in an asset group ........................ 15

2.3.1.3 Entity-wide asset groupings ....................................................................... 15

2.3.1.4 Goodwill and other assets or liabilities in asset groups .................................. 16

2.3.1.5 Cumulative translation adjustments in impairment of asset groups ................ 17

2.3.2 Estimates of future cash flows used to test a long-lived asset for recoverability ............... 18

2.3.2.1 Cash flow estimation approach ................................................................... 18

2.3.2.1.1 Consideration of taxes in cash flow estimation ..................................... 20

2.3.2.2 Probability-weighted and best estimate cash flow approaches....................... 21

2.3.2.3 Cash flow estimation period ....................................................................... 23

2.3.2.4 Asset-related expenditures for a long-lived asset in use ................................ 24

2.3.2.5 Asset-related expenditures for a long-lived asset under development ............. 25

2.3.2.6 Timing of estimates ................................................................................... 26

2.3.2.7 Effect of asset retirement obligations on cash flow estimates ........................ 27

2.3.2.8 Effect of environmental exit costs on cash flow estimates used in

the recoverability test ................................................................................ 27

2.3.2.9 Cash flow estimates for certain intangible assets .......................................... 30

2.3.2.10 Performing the test for recoverability.......................................................... 30

Contents

Financial reporting developments Impairment or disposal of long-lived assets | ii

2.4 Measuring an impairment — Step 3 ........................................................................................ 31

2.4.1 Fair value — Overview of ASC 820 ................................................................................ 32

2.4.1.1 Exit price .................................................................................................. 32

2.4.1.2 Highest and best use ................................................................................. 32

2.4.1.3 Risk premiums .......................................................................................... 33

2.4.1.4 Valuation techniques ................................................................................. 33

2.4.2 Cash flows used in the recoverability test versus those used to determine fair value ....... 33

2.4.3 Unit of valuation and unit of account ............................................................................ 34

2.4.4 Considerations in assessing appraisals ......................................................................... 35

2.4.5 Present value techniques ............................................................................................. 36

2.4.5.1 Discount rate adjustment technique ............................................................ 37

2.4.5.2 Expected present value technique ............................................................... 38

2.4.6 Considerations in developing valuation assumptions ...................................................... 40

2.4.7 Consideration of debt in the fair value of an asset group ................................................ 40

2.5 Allocation of an impairment loss ........................................................................................... 41

2.6 New cost basis ..................................................................................................................... 42

2.7 Impairment of right-of-use assets (after the adoption of ASC 842) (updated May 2023) .......... 43

2.7.1 Right-of-use assets — test for recoverability (Step 2) (updated August 2021) ................. 44

2.7.2 Right-of-use assets — measuring an impairment (Step 3) (updated August 2021) ............. 47

2.7.3 Abandonment of right-of-use assets (updated August 2021) ......................................... 50

2.8 Reporting and disclosure ...................................................................................................... 54

2.8.1 Early warning disclosures ............................................................................................. 55

3 Long-lived assets to be disposed of other than by sale ................................................ 57

3.1 Long-lived assets to be abandoned ........................................................................................ 57

3.2 Long-lived asset to be exchanged or to be distributed to owners in a spin-off ........................... 59

3.3 SEC staff views — spin-off of a subsidiary ............................................................................... 60

4 Long-lived assets to be disposed of by sale ................................................................ 61

4.1 Recognition ......................................................................................................................... 61

4.1.1 Held for sale criteria .................................................................................................... 62

4.1.2 Held for sale criteria met after the balance sheet date but before issuance

of financial statements ................................................................................................ 69

4.1.3 Grouping assets to be disposed of by sale ..................................................................... 69

4.1.3.1 Allocating goodwill to a disposal group ........................................................ 70

4.1.3.2 Reassessment of allocated goodwill to a disposal group ............................... 71

4.2 Measurement ...................................................................................................................... 72

4.2.1 ASC 820 and fair value less costs to sell ........................................................................ 73

4.2.2 Costs to sell ................................................................................................................ 73

4.2.3 Initial adjustment to fair value less cost to sell and interaction with other standards ......... 74

4.2.3.1 Individual long-lived assets......................................................................... 74

4.2.3.2 Disposal groups (updated May 2023) .......................................................... 74

4.2.3.3 SEC staff views — recording impairment losses for disposal groups ................. 76

4.2.4 Subsequent changes to fair value less cost to sell .......................................................... 77

4.2.5 Effect of a sales contract on fair value for assets held for sale........................................ 78

4.2.6 Depreciation ............................................................................................................... 78

4.2.7 Newly acquired long-lived assets to be sold ................................................................... 78

4.2.8 Accounting for foreclosed assets received in settlement of a receivable .......................... 79

Contents

Financial reporting developments Impairment or disposal of long-lived assets | iii

4.3 Changes to a plan of sale ...................................................................................................... 83

4.4 Cumulative translation adjustments and other items of accumulated other

comprehensive income in impairment of disposal groups (updated September 2022) ............ 85

4.5 Presentation and disclosure ................................................................................................. 86

5 Industry-specific considerations ................................................................................ 89

5.1 Real estate .......................................................................................................................... 89

5.1.1 Real estate developers ................................................................................................. 89

5.1.2 Real estate held for investment .................................................................................... 89

5.2 Oil and gas........................................................................................................................... 90

5.2.1 Grouping of assets ....................................................................................................... 90

5.2.2 Cash flows used to test oil and gas properties for recoverability ...................................... 90

5.2.3 Estimating fair value .................................................................................................... 91

5.2.4 Reserve estimate revisions and impairment .................................................................. 92

5.2.5 Asset retirement obligations and impairment of oil and gas properties ........................... 92

5.2.6 Oil and gas properties held for sale ............................................................................... 93

5.3 Regulated operations ........................................................................................................... 93

5.4 Not-for-profit organizations .................................................................................................. 93

5.4.1 Assets to be held and used ........................................................................................... 93

5.4.2 Presentation ............................................................................................................... 93

5.5 Mining assets ....................................................................................................................... 93

A Abbreviations used in this publication ...................................................................... A-1

B Glossary ................................................................................................................. B-1

C Index of ASC references in this publication ............................................................... C-1

D Summary of important changes ............................................................................... D-1

Contents

Financial reporting developments Impairment or disposal of long-lived assets | iv

Notice to readers:

This publication includes excerpts from and references to the Financial Accounting Standards Board

(FASB or Board) Accounting Standards Codification (Codification or ASC). The Codification uses a

hierarchy that includes Topics, Subtopics, Sections and Paragraphs. Each Topic includes an Overall

Subtopic that generally includes pervasive guidance for the Topic and additional Subtopics, as needed,

with incremental or unique guidance. Each Subtopic includes Sections that in turn include numbered

Paragraphs. Thus, a Codification reference includes the Topic (XXX), Subtopic (YY), Section (ZZ) and

Paragraph (PP).

Throughout this publication references to guidance in the Codification are shown using these reference

numbers. References are also made to certain pre-Codification standards (and specific sections or

paragraphs of pre-Codification standards) in situations in which the content being discussed is excluded

from the Codification.

This publication has been carefully prepared, but it necessarily contains information in summary form

and is therefore intended for general guidance only; it is not intended to be a substitute for detailed

research or the exercise of professional judgment. The information presented in this publication should

not be construed as legal, tax, accounting, or any other professional advice or service. Ernst & Young

LLP can accept no responsibility for loss occasioned to any person acting or refraining from action as a

result of any material in this publication. You should consult with Ernst & Young LLP or other

professional advisors familiar with your particular factual situation for advice concerning specific audit,

tax or other matters before making any decisions.

Portions of FASB publications reprinted with permission. Copyright Financial Accounting Standards Board, 801 Main Avenue, P.O.

Box 5116, Norwalk, CT 06856-5116, USA. Portions of AICPA Statements of Position, Technical Practice Aids and other AICPA

publications reprinted with permission. Copyright American Institute of Certified Public Accountants, 1345 Avenue of the Americas,

27th Floor, New York, NY 10105, USA. Copies of complete documents are available from the FASB and the AICPA.

Financial reporting developments Impairment or disposal of long-lived assets | 1

1 Overview

1.1 Introduction

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Overview and Background

General

360-10-05-2

The guidance in the Overall Subtopic is presented in the following two Subsections:

a. The General Subsections address the accounting and reporting for property, plant, and

equipment, including guidance for accumulated depreciation.

b. The Impairment or Disposal of Long-Lived Assets Subsections retain the pervasive guidance for

recognizing and measuring the impairment of long-lived assets and for long-lived assets to be

disposed of.

Impairment or Disposal of Long-Lived Assets

360-10-05-4

The Impairment or Disposal of Long-Lived Assets Subsections provide guidance for:

a. Recognition and measurement of the impairment of long-lived assets to be held and used

b. Measurement of long-lived assets to be disposed of by sale

c. Disclosures about the impairment or disposal of long-lived assets and disposals of individually

significant components of an entity.

360-10-05-5

For long-lived assets disposed of or classified as held for sale, different presentation and disclosures are

required depending on the nature of the disposal. If the long-lived assets are a significant component of an

entity, more extensive disclosures are required. Additionally, if the component of an entity meets the

definition of discontinued operation in paragraph 205-20-45-1B, an entity shall refer to Subtopic 205-20

for the presentation and disclosure requirements for discontinued operations (see the flowchart in

paragraph 360-10-55-18A for an illustration).

360-10-05-6

This Subsection provides guidance that focuses on developing estimates of future cash flows used to

test for recoverability, including the:

a. Cash flow estimation approach

b. Cash flow estimation period

c. Types of asset-related expenditures that should be considered in developing estimates of future

cash flows.

1 Overview

Financial reporting developments Impairment or disposal of long-lived assets | 2

The accounting for the impairment or disposal of long-lived assets is primarily addressed in the Impairment

or Disposal of Long-Lived Asset Subsections of ASC 360-10 (referred to simply as “ASC 360-10” in the

remainder of this publication).

This section summarizes the basic requirements of ASC 360-10. Section 2 provides more detailed

information on the recognition and measurement of impairments of long-lived assets (asset groups) held

and used, as well as estimates of future cash flows and fair value. Section 3 discusses long-lived assets to

be disposed of other than by sale (i.e., by abandonment, exchanged for a similar productive long-lived

asset, or distributed in a spin-off), and section 4 provides detailed information and practical guidance

about long-lived assets (disposal groups) that are to be disposed of by sale. Section 5 discusses industry-

specific considerations for the real estate, oil and gas, regulated industries and not-for-profit organizations.

1.2 Scope

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Scope and Scope Exceptions

General

360-10-15-1

The General Subsection of this Section establishes the pervasive scope for this Subtopic, with specific

exceptions noted in the other Subsections of this Section.

360-10-15-2

The guidance in this Subtopic applies to all entities.

Impairment or Disposal of Long-Lived Assets

360-10-15-3

The Impairment or Disposal of Long-Lived Assets Subsections follow the same Scope and Scope

Exceptions as outlined in the General Subsection of this Subtopic, see paragraph 360-10-15-1, with

specific transaction exceptions noted below.

360-10-15-4

The guidance in the Impairment or Disposal of Long-Lived Assets Subsections applies to the following

transactions and activities:

a. Except as indicated in (b) and the following paragraph, all of the transactions and activities related

to recognized long-lived assets of an entity to be held and used or to be disposed of, including:

1. Capital leases of lessees

2. Long-lived assets of lessors subject to operating leases

3. Proved oil and gas properties that are being accounted for using the successful-efforts

method of accounting

4. Long-term prepaid assets.

b. The following transactions and activities related to assets and liabilities that are considered part

of an asset group or a disposal group:

1. If a long-lived asset (or assets) is part of a group that includes other assets and liabilities not

covered by the Impairment or Disposal of Long-Lived Assets Subsections, the guidance in

the Impairment or Disposal of Long-Lived Assets Subsections applies to the group. In those

situations, the unit of accounting for the long-lived asset is its group. For a long-lived asset

1 Overview

Financial reporting developments Impairment or disposal of long-lived assets | 3

or assets to be held and used, that group is referred to as an asset group. For a long-lived

asset or assets to be disposed of by sale or otherwise, that group is referred to as a disposal

group. Examples of liabilities included in a disposal group are legal obligations that transfer

with a long-lived asset, such as certain environmental obligations, and obligations that, for

business reasons, a potential buyer would prefer to settle when assumed as part of a group,

such as warranty obligations that relate to an acquired customer base.

2. The guidance in the Impairment or Disposal of Long-Lived Assets Subsections does not

change generally accepted accounting principles (GAAP) applicable to those other individual

assets (such as accounts receivable and inventory) and liabilities (such as accounts payable,

long-term debt, and asset retirement obligations) not covered by the Impairment or Disposal

of Long-Lived Assets Subsections that are included in such groups.

Pending Content:

Transition Date: (P) December 16, 2018; (N) December 16, 2021 | Transition Guidance: 842-10-65-1

Editor’s note: The content of paragraph 360-10-15-4 will change upon the adoption of ASU 2016-02,

Leases.

The guidance in the Impairment or Disposal of Long-Lived Assets Subsections applies to the

following transactions and activities:

a. Except as indicated in (b) and the following paragraph, all of the transactions and activities related

to recognized long-lived assets of an entity to be held and used or to be disposed of, including:

1. Right-of-use assets of lessees

2. Long-lived assets of lessors subject to operating leases

3. Proved oil and gas properties that are being accounted for using the successful-efforts

method of accounting

4. Long-term prepaid assets.

b. The following transactions and activities related to assets and liabilities that are considered

part of an asset group or a disposal group:

1. If a long-lived asset (or assets) is part of a group that includes other assets and liabilities

not covered by the Impairment or Disposal of Long-Lived Assets Subsections, the

guidance in the Impairment or Disposal of Long-Lived Assets Subsections applies to the

group. In those situations, the unit of accounting for the long-lived asset is its group. For a

long-lived asset or assets to be held and used, that group is referred to as an asset group.

For a long-lived asset or assets to be disposed of by sale or otherwise, that group is

referred to as a disposal group. Examples of liabilities included in a disposal group are

legal obligations that transfer with a long-lived asset, such as certain environmental

obligations, and obligations that, for business reasons, a potential buyer would prefer to

settle when assumed as part of a group, such as warranty obligations that relate to an

acquired customer base.

2. The guidance in the Impairment or Disposal of Long-Lived Assets Subsections does not

change generally accepted accounting principles (GAAP) applicable to those other

individual assets (such as accounts receivable and inventory) and liabilities (such as

accounts payable, long-term debt, and asset retirement obligations) not covered by the

Impairment or Disposal of Long-Lived Assets Subsections that are included in such groups.

1 Overview

Financial reporting developments Impairment or disposal of long-lived assets | 4

360-10-15-5

The guidance in the Impairment or Disposal of Long-Lived Assets Subsections does not apply to the

following transactions and activities:

a. Goodwill

b. Intangible assets not being amortized that are to be held and used

c. Servicing assets

d. Financial instruments, including investments in equity securities accounted for under the cost or

equity method

e. Deferred policy acquisition costs

f. Deferred tax assets

g. Unproved oil and gas properties that are being accounted for using the successful-efforts method

of accounting

h. Oil and gas properties that are accounted for using the full-cost method of accounting as

prescribed by the Securities and Exchange Commission (SEC) (see Regulation S-X, Rule 4-10,

Financial Accounting and Reporting for Oil and Gas Producing Activities Pursuant to the Federal

Securities Laws and the Energy Policy and Conservation Act of 1975)

i. Certain other long-lived assets for which the accounting is prescribed elsewhere in the standards:

1. For guidance on financial reporting in the record and music industry, see Topic 928.

2. For guidance on financial reporting in the broadcasting industry, see Topic 920.

3. For guidance on accounting for the costs of computer software to be sold, leased, or

otherwise marketed, see Subtopic 985-20.

4. For guidance on accounting for abandonments and disallowances of plant costs for regulated

entities, see Subtopic 980-360.

ASC 360-10 applies to recognized individual long-lived assets of a business enterprise and not-for-profit

organizations to be held and used or to be disposed of, as well as to groups of assets, which may include assets

and liabilities other than long-lived assets. However, these groups must also contain long-lived assets. Following

the adoption of ASU 2016-02, lessees’ right-of-use (ROU) assets, for both operating and finance leases,

are subject to the impairment guidance in ASC 360-10. Note that the impairment guidance in ASC 360-10

applies to all long-lived assets, including definite-lived intangible assets, as noted in ASC 350-30:

Excerpt from Accounting Standards Codification

Intangibles—Goodwill and Other — General Intangibles Other Than Goodwill

Subsequent Measurement

350-30-35-14

An intangible asset that is subject to amortization shall be reviewed for impairment in accordance with

the Impairment or Disposal of Long-Lived Assets Subsections of Subtopic 360-10 by applying the

recognition and measurement provisions in paragraphs 360-10-35-17 through 35-35. In accordance

with the Impairment or Disposal of Long–Lived Assets Subsections of Subtopic 360-10, an impairment

loss shall be recognized if the carrying amount of an intangible asset is not recoverable and its carrying

amount exceeds its fair value. After an impairment loss is recognized, the adjusted carrying amount of

the intangible asset shall be its new accounting basis. Subsequent reversal of a previously recognized

impairment loss is prohibited.

1 Overview

Financial reporting developments Impairment or disposal of long-lived assets | 5

The exclusions noted in ASC 360-10-15-5 should not be interpreted to imply that entire industries or types of

entities (e.g., banking, insurance, regulated, record and music, software, oil and gas, real estate) are excluded

from the scope of ASC 360-10. The exclusions apply only to long-lived assets whose accounting is prescribed

by other generally accepting accounting principles (GAAP). It is possible for an entity to have some of its long-

lived assets accounted for under ASC 360-10 and other long-lived assets accounted for under other GAAP.

1.3 Long-lived assets to be held and used

The following are the required steps to identify, recognize and measure the impairment of a long-lived

asset (group) to be held and used:

1. Indicators of impairment — Consider whether indicators of impairment are present.

2. Test for recoverability — If indicators are present, perform a recoverability test by comparing the sum

of the estimated undiscounted future cash flows attributable to the long-lived asset (group) in question

to its carrying amount (as a reminder, entities cannot record an impairment for a held and used asset

unless the asset first fails this recoverability test).

3. Measurement of an impairment — If the undiscounted cash flows used in the test for recoverability

are less than the carrying amount of the long-lived asset (group), determine the fair value of the long-

lived asset (group) and recognize an impairment loss if the carrying amount of the long-lived asset

(group) exceeds its fair value.

1.3.1 Indicators of impairment — Step 1

A long-lived asset (group) that is held and used must be reviewed for impairment whenever events or

changes in circumstances indicate that the carrying amount of the long-lived asset (group) might not be

recoverable (i.e., information indicates that an impairment might exist). As a result, entities are not

required to perform an impairment analysis (i.e., test the asset (group) for recoverability and potentially

measure an impairment loss) if indicators of impairment are not present. Instead, entities would assess

the need for an impairment write-down only if an indicator of impairment (e.g., a significant decrease in

the market value of a long-lived asset (group)) is present. Entities are responsible for routinely assessing

whether impairment indicators are present and should have systems or processes to assist in the

identification of potential impairment indicators.

1.3.2 Test for recoverability — Step 2

If impairment indicators are present or if other circumstances indicate that an impairment may exist,

management must then determine whether an impairment loss should be recognized. An impairment loss

can be recognized for a long-lived asset (group) that is held and used only if the sum of its estimated

future undiscounted cash flows used to test for recoverability is less than its carrying value.

Estimates of future cash flows used to test a long-lived asset (group) for recoverability include only the

future cash flows (cash inflows and associated cash outflows) that are directly associated with and that

are expected to arise as a direct result of the use and eventual disposition of the long-lived asset (group).

Estimates of future cash flows are based on an entity’s own assumptions about its use of a long-lived

asset (group). These entity-specific assumptions could give rise to different cash flows than the cash flows

that an entity would use for purposes of measuring fair value in Step 3.

The cash flow estimation period is based on the remaining useful life of the long-lived asset (group) to the

entity. When long-lived assets are grouped (see further discussion regarding the grouping of long-lived

assets in section 2.3.1) for purposes of performing the recoverability test, the remaining useful life of the

asset group is based on the useful life of the primary asset. The primary asset of the asset group is the

principal long-lived tangible asset being depreciated (or identifiable intangible asset being amortized) that

is the most significant component asset from which the group derives its cash-flow-generating capacity.

1 Overview

Financial reporting developments Impairment or disposal of long-lived assets | 6

Estimates of future cash flows used to test the recoverability of a long-lived asset (group) that is in use,

including a long-lived asset (group) for which development is substantially complete, should be based on

the existing service potential of the asset (group) at the date tested. Existing service potential

encompasses the long-lived asset’s remaining estimated useful life, cash flow generating capacity and for

tangible assets, the physical output capacity. The estimated cash flows include cash flows associated with

future expenditures necessary to maintain the existing service potential, including those that replace the

service potential of component parts (e.g., the roof of a building), but they should not include cash flows

associated with future capital expenditures that would increase the service potential.

The guidance in ASC 360-10 permits (and encourages) but does not require the use of a probability-

weighted cash flow estimation approach in performing the recoverability test.

1.3.3 Measurement of an impairment loss — Step 3

If it is determined that a long-lived asset (group) is not recoverable, an impairment loss would be

calculated based on the excess of the carrying amount of the long-lived asset (group) over the fair value of

the long-lived asset (group).

Fair value used in Step 3 is determined using the guidance in ASC 820. ASC 820 defines fair value as “the

price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between

market participants at the measurement date.”

The guidance in ASC 820 is principles-based guidance intended to provide a framework for measuring fair

value in US GAAP. This framework is based on a number of key concepts including unit of account, exit

price, valuation premise, highest and best use, principal market, market participant assumptions and the fair

value hierarchy, which form the foundation of the fair value measurement approach to be utilized for

financial reporting purposes. ASC 820 includes a single definition of fair value that should be used for

financial reporting purposes, provides a framework for applying this definition and requires numerous

disclosures about the use of fair value measurements in the financial statements. The guidance in ASC 820

incorporates financial theory and valuation techniques but is focused solely on how these concepts should

be applied when determining fair value for financial reporting purposes.

We have provided information regarding the application of ASC 820 to long-lived assets being evaluated

for impairment in section 2.4. Additional information regarding fair value measurements under ASC 820

can be found in our Financial reporting developments (FRD) publication, Fair value measurement.

1.3.4 Allocation of an impairment loss

ASC 360-10 provides specific guidance on the allocation of an impairment loss to an asset group. It requires

that an impairment loss reduce only the carrying amounts of the assets of the group that are covered by

ASC 360-10. Thus, in no circumstance will goodwill, indefinite-lived intangibles, other assets excluded

from the scope of ASC 360-10 or liabilities be affected by an impairment loss recognized under this

guidance, even if those assets or liabilities are included in the asset group being tested for impairment.

The impairment loss will reduce the carrying amount of the long-lived assets of a group covered by

ASC 360-10 on a pro rata basis using the relative carrying amounts of those assets. However, the

carrying amount of a long-lived asset of the group must not be reduced below its fair value.

1.3.5 Reporting and disclosure of impairments

An impairment loss is reported as a component of income from continuing operations before income

taxes. In addition, an entity that reports an impairment loss is also required to disclose the following

information in the notes to the financial statements:

• A description of the long-lived asset (group) that is impaired and the facts and circumstances leading

to the impairment

1 Overview

Financial reporting developments Impairment or disposal of long-lived assets | 7

• The amount of the impairment loss and the caption in the income statement in which the loss is

aggregated, if not presented separately on the face of the income statement

• The method(s) used to determine fair value

• If applicable, the segment in which the impaired long-lived asset (group) is reported

1.4 Long-lived assets to be disposed of other than by sale

A long-lived asset (group) to be disposed of other than by sale (e.g., by abandonment, in exchange for a

similar productive asset or in a distribution to owners in a spin-off) would continue to be classified as held

and used until the long-lived asset (group) is disposed.

1.5 Long-lived assets to be disposed of by sale

1.5.1 Held for sale criteria

A long-lived asset (or disposal group) to be disposed of by sale (including an asset group considered a

component of an entity) is considered held for sale when all of the following criteria for a qualifying plan

of sale are met:

• Management, having the authority to approve the action, commits to a plan to sell the asset or

disposal group

• The asset or disposal group is available for immediate sale (i.e., a seller currently has the intent and

ability to transfer the asset (group) to a buyer) in its present condition, subject only to conditions

that are usual and customary for sales of such assets or disposal groups

• An active program to locate a buyer and other actions required to complete the plan to sell have

been initiated

• The sale of the asset or disposal group is probable (i.e., likely to occur) and the transfer is expected

to qualify for recognition as a completed sale within one year

• The long-lived asset or disposal group is being actively marketed for sale at a price that is reasonable

in relation to its current fair value

• Actions necessary to complete the plan indicate that it is unlikely significant changes to the plan will

be made or that the plan will be withdrawn

The FASB permits an exception to the one-year requirement (in the fourth bullet above) if events or

circumstances beyond an entity’s control extend the period of time required to sell the assets beyond one

year (refer to section 4.1.1 for further discussion).

The disposal group qualifies for reporting as a discontinued operation if it: (1) is a component of an entity

(or group of components), (2) meets the held for sale criteria as prescribed by ASC 205-20-45-1E, is

disposed of by sale or is disposed of other than by sale (e.g., abandonment), and (3) represents a

strategic shift that has (or will have) a major effect on an entity’s operations and financial results. Refer

to our FRD, Discontinued operations — Accounting Standards Codification 205-20, for further guidance

on discontinued operations classified as held for sale.

1 Overview

Financial reporting developments Impairment or disposal of long-lived assets | 8

1.5.2 Measurement

A long-lived asset (disposal group) classified as held for sale is initially measured at the lower of its carrying

amount or fair value less cost to sell. A loss is recognized for any initial adjustment of the carrying amount

of the long-lived asset or disposal group to its fair value less cost to sell in the period the held for sale

criteria are met. The fair value less cost to sell of the long-lived asset (disposal group) is required to be

assessed each reporting period it remains classified as held for sale. Subsequent changes in the long-lived

asset’s fair value less cost to sell (increase or decrease) would be reported as an adjustment to its carrying

amount, except that the adjusted carrying amount must not exceed the carrying amount of the long-lived

asset at the time it was initially classified as held for sale. Gains or losses not previously recognized

resulting from the sale of a long-lived asset are recognized on the date of sale. A long-lived asset or long-

lived assets within a disposal group is not depreciated or amortized when classified as held for sale.

The carrying amount of any asset that is not covered by ASC 360-10, including goodwill, that is included

in a disposal group classified as held for sale, should be adjusted in accordance with generally accepted

accounting principles (e.g., inventory in accordance with ASC 330 or goodwill in accordance with ASC 350),

before measuring the fair value less cost to sell of the disposal group.

1.5.3 Grouping of assets held for sale

A disposal group includes only assets to be disposed of together as a group in a single transaction and

liabilities directly associated with those that will be transferred in that transaction. Examples of such

liabilities include, but are not limited to, environmental obligations that transfer with the asset, warranty

obligations that relate to an acquired customer base and assumable debt with an interest rate below the

current market rate.

1.5.4 Changes to a plan of sale

If circumstances arise that were previously considered unlikely and an entity subsequently decides not to

sell a long-lived asset (disposal group) that is classified as held for sale, the long-lived asset (disposal

group) would be reclassified as held and used. The guidance in ASC 360-10 requires that a long-lived

asset (or the long-lived assets of a disposal group) that is reclassified from held for sale to held and used

be measured at the time of the reclassification individually at the lower of its (a) carrying amount before it

was classified as held for sale, adjusted for any depreciation (amortization) expense or impairment losses

that would have been recognized had the asset (group) been continuously classified as held and used or

(b) fair value at the date of the subsequent decision not to sell. The effect of any required adjustment would

be reflected in income from continuing operations at the date of the decision not to sell. One interesting

result of applying the change to a plan of sale provision is that if a held for sale long-lived asset (disposal

group) is measured at its fair value less costs to sell and then remeasured to its fair value because of a

change to a plan of sale, there will be an immediate write-up in the carrying value of the long-lived asset

(group) reflected in income as a result of the elimination of the costs to sell from the measurement of the

long-lived asset (group). In addition, a description of the facts and circumstances leading to the decision

to change the plan to sell the long-lived asset (disposal group) and its effects on the results of operations

for the period and any prior periods must be disclosed.

Financial reporting developments Impairment or disposal of long-lived assets | 9

2 Long-lived assets to be held and used

2.1 Overview

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Subsequent Measurement

Measurement of an Impairment Loss

360-10-35-15

There are unique requirements of accounting for the impairment or disposal of long-lived assets to be

held and used or to be disposed of. Although this guidance deals with matters which may lead to the

ultimate disposition of assets, it is included in this Subsection because it describes the measurement and

classification of assets to be held and used and assets held for disposal before actual disposition and

derecognition. See the Impairment or Disposal of Long-Lived Assets Subsection of Section 360–10–40

for a discussion of assets or asset groups for which disposition has taken place in an exchange or

distribution to owners.

Long-Lived Assets Classified as Held and Used

360-10-35-16

This guidance addresses how long-lived assets or asset groups that are intended to be held and used in

an entity’s business shall be reviewed for impairment.

360-10-35-17

An impairment loss shall be recognized only if the carrying amount of a long-lived asset (asset group)

is not recoverable and exceeds its fair value. The carrying amount of a long-lived asset (asset group) is

not recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use

and eventual disposition of the asset (asset group). That assessment shall be based on the carrying

amount of the asset (asset group) at the date it is tested for recoverability, whether in use (see paragraph

360-10-35-33) or under development (see paragraph 360-10-35-34). An impairment loss shall be measured

as the amount by which the carrying amount of a long-lived asset (asset group) exceeds its fair value.

This section discusses the accounting for the impairment of long-lived assets to be held and used. Long-

lived assets that are held and used are those assets that an entity uses in its operations and for which the

held for sale criteria (discussed in section 4.1.1) have not been met.

The following are the required steps to identify, recognize and measure the impairment of a long-lived

asset (group) to be held and used:

1. Indicators of impairment — Consider whether indicators of impairment are present.

2. Test for recoverability — If indicators are present, perform a recoverability test by comparing the sum

of the estimated undiscounted future cash flows attributable to the assets in question to their

carrying amounts (as a reminder, entities cannot record an impairment for a held and used asset

unless the asset first fails this recoverability test).

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 10

3. Measurement of an impairment — If the undiscounted cash flows used in the test for recoverability

are less than the carrying amount of the long-lived asset (group), determine the fair value of the long-

lived asset (group) and recognize an impairment loss if the carrying amount of the long-lived asset

(group) exceeds its fair value.

2.2 Indicators of impairment — Step 1

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Subsequent Measurement

360-10-35-21

A long-lived asset (asset group) shall be tested for recoverability whenever events or changes in

circumstances indicate that its carrying amount may not be recoverable. The following are examples

of such events or changes in circumstances:

a. A significant decrease in the market price of a long-lived asset (asset group)

b. A significant adverse change in the extent or manner in which a long-lived asset (asset group) is

being used or in its physical condition

c. A significant adverse change in legal factors or in the business climate that could affect the value

of a long-lived asset (asset group), including an adverse action or assessment by a regulator

d. An accumulation of costs significantly in excess of the amount originally expected for the

acquisition or construction of a long-lived asset (asset group)

e. A current-period operating or cash flow loss combined with a history of operating or cash flow

losses or a projection or forecast that demonstrates continuing losses associated with the use of a

long-lived asset (asset group)

f. A current expectation that, more likely than not, a long-lived asset (asset group) will be sold or

otherwise disposed of significantly before the end of its previously estimated useful life. The term

more likely than not refers to a level of likelihood that is more than 50 percent.

ASC 360-10 requires that a long-lived asset (group) be reviewed for impairment only when events or

changes in circumstances indicate that the carrying amount of the long-lived asset (group) might not be

recoverable. Accordingly, entities do not need to routinely perform tests of recoverability. However,

entities are responsible for routinely assessing whether impairment indicators are present and should

have systems or processes to assist in the detection of impairment indicators.

To assist management in determining when long-lived assets (groups) should be evaluated for impairment,

ASC 360-10-35-21 above provides examples of events or changes in circumstances that indicate the

carrying amount of a long-lived asset (group) might not be recoverable and thus an impairment might exist.

The list above is not meant to be all-inclusive and there might be other situations, including circumstances that

are particular to an entity’s business or industry that indicate an impairment might exist or that the carrying

amount of a long-lived asset (group) might not be recoverable. In the Background Information and Basis for

Conclusions to Financial Accounting Standards Statement No. 144, Accounting for the Impairment or

Disposal of Long-Lived Assets (Statement No. 144), the FASB further emphasizes that “existing information

and analyses developed for management review of the entity and its operations generally will be the

principal evidence needed to determine when an impairment exists” (Statement No. 144, paragraph B16).

Therefore, entities should consider the FASB’s list of indicators as well as other events or circumstances that

they are aware of that suggest the carrying amount of a long-lived asset (group) might not be recoverable

to determine whether a recoverability test must be performed.

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 11

In addition to the indicators of impairment noted in ASC 360-10-35-21, the following indicators also may

be relevant:

• A significant drop in the stock price of the entity

• An impairment of goodwill and other non-amortizing intangibles under ASC 350. This would be a

particularly relevant indicator when the intangible relates to or is used by an asset group containing

other long-lived assets

• Insufficient rental demand for a rental project currently under construction

It should be noted that for purposes of applying the impairment indicators to a particular circumstance, it is

possible that impairments result from changes in economic conditions or other factors that develop over

time. For example, industry trends that indicate a potential decrease in demand for an entity’s product do not

always develop to the point where an impairment might be indicated within one reporting cycle. Additionally,

consider a situation where the trend in sales has reflected a 5% average annual decrease for the last few

years, or where the market value of the entity’s principal products has declined steadily for the last several

years. These examples illustrate that the application of the above impairment indicators to a given

circumstance may have to be considered over a continuum rather than a relatively short period of time.

As noted above, management’s ongoing analysis and review of the entity and its operations should provide

a basis for determining whether there are any indicators of impairment. In conjunction with that review,

management should be alert to potential impairment indicators unique to its circumstances, as well as

other events and changes in circumstances that might indicate that an impairment exists. For smaller

entities and those with centralized operations, the information-gathering aspects of this process should not

be onerous because of management’s in-depth knowledge of all aspects of the business. However, for

larger entities or those with decentralized operations, this information gathering process could be more

challenging. Such entities may need to establish a system for communicating with managers at their

various locations to determine whether indicators of impairment are present and to ensure that local

management has assessed the need to record an impairment loss and has communicated the results of

that assessment to corporate personnel responsible for preparing the consolidated financial statements. To

facilitate this process, management may wish to include a schedule in the internal reporting package to be

completed by each business unit that lists the indicators of impairment described in ASC 360-10 and other

events or circumstances specific to its business or industry that might indicate an impairment exists. The

completed schedule could indicate whether any indicators of impairment are present and whether the need

to record an impairment loss has been considered. This process should provide corporate management

with assurance that throughout the organization appropriate consideration has been given to identifying

situations that imply a long-lived asset (group) might be impaired.

2.2.1 Depreciation estimates

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Subsequent Measurement

360-10-35-22

When a long-lived asset (asset group) is tested for recoverability, it also may be necessary to review

depreciation estimates and method as required by Topic 250 or the amortization period as required by

Topic 350. Paragraphs 250-10-45-17 through 45-20 and 250-10-50-4 address the accounting for

changes in estimates, including changes in the method of depreciation, amortization, and depletion.

Paragraphs 350-30-35-1 through 35-5 address the determination of the useful life of an intangible

asset. Any revision to the remaining useful life of a long-lived asset resulting from that review also shall

be considered in developing estimates of future cash flows used to test the asset (asset group) for

recoverability (see paragraphs 360-10-35-31 through 35-32). However, any change in the accounting

method for the asset resulting from that review shall be made only after applying this Subtopic.

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 12

We believe that management should closely evaluate depreciation estimates when impairment indicators

exist and, in turn, the asset (group) is tested for recoverability. If management determines that the

depreciation estimate should be changed, it should use the revised depreciation estimates for the

undiscounted cash flow projections in conjunction with testing the asset for recoverability. For example,

if management determines that the remaining useful life of an asset (or the primary asset in the asset

group) is 7 years instead of 10, the cash flow projections used in the recoverability test should be for

7 years only, the new estimate of the remaining useful life. In accordance with ASC 360-10-35-22 above,

changes to prospective depreciation or amortization expense should be made only after completing the

impairment analysis.

2.3 Test for recoverability—Step 2

If any of the impairment indicators are present, or if other circumstances indicate that an impairment

might exist, management must then perform Step 2, the recoverability test, to determine whether an

impairment loss should be measured. In other words, before measuring an impairment, an entity must

first determine whether the long-lived asset (group) is recoverable. The following steps are performed in

making that determination:

1. Group long-lived assets and, if applicable, liabilities at the lowest level for which there are identifiable

cash flows that are largely independent of the cash flows of the other assets and liabilities. (See

further discussion of asset groupings in section 2.3.1.)

2. Estimate the future net undiscounted cash flows expected to be generated from the use of the long-

lived asset (group) and its eventual disposal. (See further discussion of cash flow estimates in

section 2.3.2.)

3. Compare the estimated undiscounted cash flows to the carrying amount of the long-lived asset (group):

a. If the estimated undiscounted cash flows exceed the carrying amount (i.e., net book value) of the

long-lived asset (group), the long-lived asset (group) is recoverable; therefore, an impairment

does not exist and a loss cannot be recognized. However, as discussed above, given the existence

of the indicators of impairment, it may be appropriate for the entity to review its depreciation

policies for the long-lived asset (group) (e.g., reduce the estimated remaining useful life or

salvage value of the assets).

b. If the estimated undiscounted cash flows are less than the carrying amount of the long-lived asset

(group), the long-lived asset (group) is not recoverable; therefore, the fair value of the long-lived

asset (group) must be determined.

All of the above steps are subjective and will require judgment.

2.3.1 Grouping long-lived assets to be held and used

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Subsequent Measurement

360-10-35-23

For purposes of recognition and measurement of an impairment loss, a long-lived asset or assets shall

be grouped with other assets and liabilities at the lowest level for which identifiable cash flows are

largely independent of the cash flows of other assets and liabilities. However, an impairment loss, if

any, that results from applying this Subtopic shall reduce only the carrying amount of a long-lived

asset or assets of the group in accordance with paragraph 360-10-35-28.

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 13

Each time an entity performs a recoverability test, it should assess whether its grouping of long-lived

assets continues to be appropriate. Significant changes to the planned use of the individual assets of the

group might indicate that the related asset grouping may have changed.

The FASB acknowledges that grouping assets requires a significant amount of judgment. As noted above,

asset groups may include assets and liabilities outside the scope of ASC 360-10 (for example, goodwill —

if certain conditions, discussed later, are met — and other non-amortizing intangible assets). In general,

assets should be grouped when they are used together, that is, when they are part of the same group of

assets and are used together to generate joint cash flows. If assets and/or liabilities are grouped for

purposes of a test for recoverability, they are referred to as an “asset group.” The Codification states the

following acknowledging the need for judgment:

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Implementation Guidance and Illustrations

360-10-55-35

Varying facts and circumstances will inevitably justify different groupings of assets for impairment

review. While grouping at the lowest level for which there are identifiable cash flows for recognition

and measurement of an impairment loss is understood, determining that lowest level requires

considerable judgment.

ASC 360-10-55-36 provides an example of the judgment used in grouping assets for impairment review,

which is the basis for Illustration 2-1.

Illustration 2-1: Grouping assets for impairment review

An entity operates a bus entity that provides service under contract with a municipality that requires

minimum service on each of five separate routes. Assets devoted to serving each route and the cash

flows from each route are discrete. One of the routes operates at a significant deficit that results in the

inability to recover the carrying amounts of the dedicated assets. The five bus routes would be an

appropriate level at which to group assets to test for and measure impairment because the entity does

not have the option to curtail any one bus route.

In other words, because the entity does not have the ability to curtail the unprofitable route (i.e., the entity

is contractually obligated to the municipality to operate all five routes), the cash flows of the unprofitable

route are not independent of the cash flows of the other four routes. Conversely, if the five routes were

operated at the sole discretion of the bus entity (i.e., not under a contract with the city) and the entity

decided to continue to operate the unprofitable route, its cash flows would be evaluated independently

of the other routes and appropriate write-downs, if necessary, would be made. Alternatively, if the

entity planned to re-deploy the long-lived assets serving the unprofitable route and evidence (i.e., the

undiscounted cash flows of the redeployed asset group) indicated that the carrying amount of such long-

lived assets would be recovered through redeployment, a write-down would not be necessary.

As discussed above, determining at what level the grouping of the long-lived assets is to be made will

require appropriate consideration of the individual facts and circumstances and an understanding of the

entity’s business. The following illustrates a situation where it might be appropriate to group long-lived

assets at a higher level than the lowest level for which cash flows are available.

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 14

Illustration 2-2: Grouping long-lived assets to be held and used

Fast Food operates a chain of restaurants located in each major city throughout the Northeast. Fast

Food’s marketing strategy provides that one restaurant in each of the major cities test markets all new

products before those products are introduced at the other restaurant locations within a city and that

the new-product restaurant offers product prices that are significantly below the prices offered at the

other locations. The entity demonstrates that the “loss-leader” restaurant strategy enables the

surrounding locations to draw on a significantly larger customer base. Each of the other restaurants in the

city (i.e., other than the loss-leader) is highly profitable and generating significant cash flows. In this case,

considering the restaurants in each city as a group for evaluating impairment may be appropriate because

the cash flows of each individual restaurant are not independent of those of the other restaurants in the city.

Another example of the judgment involved in the grouping process is an entity that is vertically integrated,

with goods produced at the subsidiary level that are sold to the parent entity. This situation might be

further complicated if the goods produced are not only sold to the parent entity, but also are sold to third-

party customers. In these circumstances, entities will need to make the grouping decision based on their

particular situation.

The flexibility accorded by ASC 360-10 in determining long-lived asset groupings will require management

to carefully consider the individual facts and circumstances surrounding its operating environment and

production processes and to exercise significant judgment. An understanding of how management views

the business will provide valuable input in making sound asset grouping decisions. From the standpoint of

the time and costs associated with determining asset groupings, challenging whether economic reasons

coupled with business strategies support a higher level of asset groupings often will prove beneficial.

For example, if retail outlets are dependent on regional distribution centers that provide warehousing,

ordering, inventory levels, advertising, accounting and other administrative services, it might be appropriate

to group retail outlets that are served by a regional distribution center rather than by individual retail outlet.

On the other hand, considering four hotels as a group for purposes of evaluating impairment merely because

the hotels share a common reservation system likely would not be appropriate.

2.3.1.1 Debt in asset groups

Generally, debt should not be included in an asset group because the lowest level of identifiable cash flows

will typically not include cash flows associated with debt (i.e., the principal payments associated with the

debt). Further, the cash flows associated with debt principal payments are typically easy to identify;

therefore, most entities will be able to eliminate the cash flows associated with debt from the cash flows

of other assets and liabilities.

However, in rare instances, if the lowest level of identifiable cash flows includes cash flows associated with

debt principal payments and it is not practical to eliminate those cash flows (which would be more likely to

occur when the asset group is a business or reporting unit), then the debt should be included in the asset

group (i.e., netted with the carrying amounts of the assets of the group) so as to maintain an appropriate

comparison. This basis adjustment provides the same result as if the debt principal payments have been

excluded (e.g., debt with a carrying value of $100 would have undiscounted cash flows of $100). As a

reminder, the guidance in ASC 360-10 prohibits the inclusion of interest expense in assessing the

recoverability of long-lived assets (see ASC 360-10-35-29 for further discussion of interest). Consider the

following illustration:

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 15

Illustration 2-3: Debt in asset groups

Assume an entity can identify cash flows associated with an individual truck being tested for recoverability.

Also assume that the truck was financed with proceeds from debt that has an outstanding balance

when the truck is tested for recoverability. Because the entity can separately identify the cash flows

associated with the individual truck (e.g., freight, maintenance, truck driver salary) from the cash flows

of the debt, the carrying amount of the debt would not be included in the asset group and the cash

flows related to the debt would not be included in the cash flow estimates.

2.3.1.2 Impairment indicators for individual assets in an asset group

If there is an impairment indicator associated with an individual long-lived asset that is included in an

asset group, an entity should consider the significance of that individual asset to the asset group as a

whole before proceeding with the recoverability test. For instance, if a personal computer is included in an

asset group with other assets of a manufacturing facility and it is probable that the computer will be sold

before the end of its useful life (and it is not probable that the other long-lived assets of the asset groups

will be sold), an entity may not need to perform a recoverability test, because the individual computer is

clearly inconsequential to the asset group as a whole. However, the entity should evaluate the propriety of

the computer’s estimated useful life and salvage value and also assess whether the computer should be

classified as held for sale. See section 4.1.1 regarding the criteria that must be met in order to classify an

asset as held for sale.

2.3.1.3 Entity-wide asset groupings

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Subsequent Measurement

360-10-35-24

In limited circumstances, a long-lived asset (for example, a corporate headquarters facility) may not

have identifiable cash flows that are largely independent of the cash flows of other assets and liabilities

and of other asset groups. In those circumstances, the asset group for that long-lived asset shall

include all assets and liabilities of the entity.

360-10-35-25

In limited circumstances, an asset group will include all assets and liabilities of the entity. For example,

the cost of operating assets such as corporate headquarters or centralized research facilities may

be funded by revenue-producing activities at lower levels of the entity. Accordingly, in limited

circumstances, the lowest level of identifiable cash flows that are largely independent of other asset

groups may be the entity level. See Example 4 (paragraph 360-10-55-35).

Certain long-lived assets do not have identifiable cash flows that are independent of the cash flows of

other assets and liabilities and cannot be identified with a specific asset group that has identifiable cash

flows. For example, the costs of administering a museum may exceed the admission fees charged but the

organization may fund the cash flow deficit with unrestricted contributions, or the cost of operating

assets such as a corporate headquarters or centralized research facilities are typically funded by revenue-

producing activities at lower levels of the enterprise.

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 16

In the above situations, those long-lived assets generally should be evaluated for impairment on an entity-

wide level. If grouped at the entity level, management should estimate whether the entity as a whole will

generate cash flows sufficient to recover the carrying amount of all the assets (liabilities) of an entity. As a

result, in many instances it will not be appropriate to go on to Step 3 for corporate level assets (e.g., an

entity-wide enterprise planning computer system, corporate headquarters) because the entity’s long-lived

assets are recoverable on an entity-wide basis. However, if an entity owns the building in which its

corporate headquarters are located and decides to vacate the entire building and lease it to a third party,

the asset would no longer be an entity-wide asset. Instead, recoverability most likely would be assessed

based on the building itself.

2.3.1.4 Goodwill and other assets or liabilities in asset groups

Excerpt from Accounting Standards Codification

Property, Plant, and Equipment — Overall

Subsequent Measurement

360-10-35-26

Goodwill shall be included in an asset group to be tested for impairment under this Subtopic only if the

asset group is or includes a reporting unit. Goodwill shall not be included in a lower-level asset group

that includes only part of a reporting unit. Estimates of future cash flows used to test that lower-level

asset group for recoverability shall not be adjusted for the effect of excluding goodwill from the group.

The term reporting unit is defined in Topic 350 as the same level as or one level below an operating

segment. That Topic requires that goodwill be tested for impairment at the reporting unit level.

360-10-35-27

Other than goodwill, the carrying amounts of any assets (such as accounts receivable and inventory)

and liabilities (such as accounts payable, long-term debt, and asset retirement obligations) not covered

by this Subtopic that are included in an asset group shall be adjusted in accordance with other applicable

generally accepted accounting principles (GAAP) before testing the asset group for recoverability.

Paragraph 350-20-35-31 requires that goodwill be tested for impairment only after the carrying

amounts of the other assets of the reporting unit, including the long-lived assets covered by this

Subtopic, have been tested for impairment under other applicable accounting guidance.

Intangibles—Goodwill and Other — Goodwill

Subsequent Measurement

350-20-35-31

If goodwill and another asset (or asset group) of a reporting unit are tested for impairment at the same

time, the other asset (or asset group) shall be tested for impairment before goodwill. For example, if a

significant asset group is to be tested for impairment under the Impairment or Disposal of Long-Lived

Assets Subsections of Subtopic 360-10 (thus potentially requiring a goodwill impairment test), the

impairment test for the significant asset group would be performed before the goodwill impairment

test. If the asset group was impaired, the impairment loss would be recognized prior to goodwill being

tested for impairment.

Sometimes long-lived assets (groups) to be held and used (including finite-lived intangible assets),

indefinite-lived intangible assets and goodwill (when the long-lived asset group is or includes a reporting

unit) may all need to be tested for impairment at the same time (e.g., due to an impairment indicator that

affects all of them). If long-lived assets tested for impairment under ASC 360-10 are grouped at or above

the reporting unit level, then goodwill, if any, of that reporting unit should be included in the asset group

in performing the recoverability test. If the asset group only includes a part of the reporting unit, goodwill

would not be allocated to the asset group in performing the recoverability test.

2 Long-lived assets to be held and used

Financial reporting developments Impairment or disposal of long-lived assets | 17

When goodwill and indefinite lived intangibles are included in the long-lived asset group being tested for

impairment, the indefinite-lived intangible assets are tested for impairment in accordance with ASC 350-

30 first, then the long-lived assets (groups) are tested for impairment in accordance with ASC 360-10,

and goodwill is tested for impairment at the reporting unit level in accordance with ASC 350-20 last. The

reason the order is important is because the impairment test of long-lived assets (groups) under ASC

360-10 and goodwill under ASC 350-20 is dependent on the carrying amounts of the underlying assets

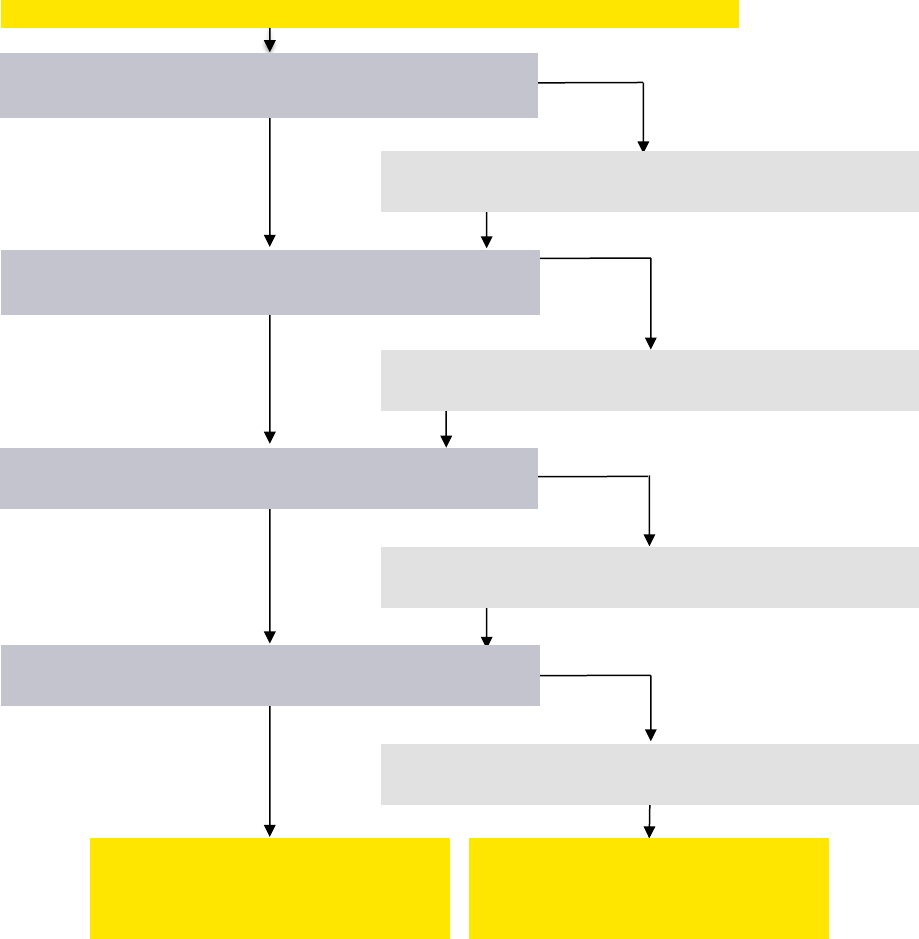

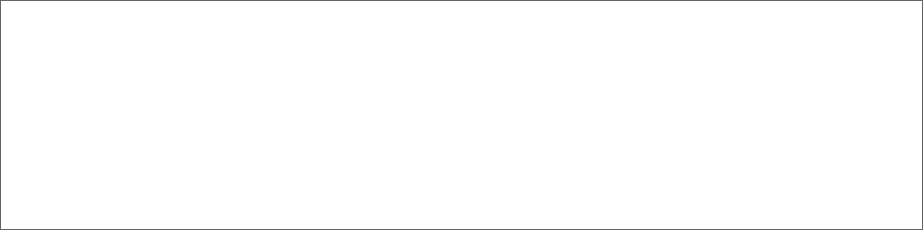

first being properly adjusted for impairment. The graphic below summarizes the order in which assets

generally need to be tested for impairment and the frequency of those tests.

The guidance regarding assigning goodwill to an asset group that is held and used differs from the guidance

in ASC 350 regarding assigning goodwill to a disposal group that is classified as held for sale (as discussed

later in section 4.1.3.1). Under ASC 350, goodwill must be allocated to a disposal group that constitutes

a part of a reporting unit if the disposal group constitutes a business. However, for asset groups that are

being held and used, goodwill may not be included in an asset group when the assets are grouped below

the reporting unit level, even if the asset group constitutes a business. Further, when an asset group within a

reporting unit is held and used, any goodwill assigned to the reporting unit is tested last (i.e., after adjusting

any assets and liabilities not subject to ASC 360-10 in accordance with ASC 360-10-35-27 and testing

long-lived assets subject to ASC 360-10).

See section 4.2.3.2 for a discussion on how the order of impairment tests differs when a long-lived asset

(group) is held for sale.

2.3.1.5 Cumulative translation adjustments in impairment of asset groups

When an asset group is held and used, the carrying amount of that asset group generally would not

include any cumulative translation adjustments associated with the group because the entity would not

have committed to a plan that would cause the cumulative translation adjustments to be reclassified to

earnings. Refer to section 4.4, Cumulative translation adjustments in impairment of disposal groups, for

considerations for cumulative translation adjustments when evaluating a disposal group for impairment.

3

2

Indefinite-lived intangible assets (ASC 350-30)*

► Annually, and more frequently if impairment indicators exist

1

Long-lived assets to be held and used (ASC 360-10)

► When impairment indicators exist

Goodwill (ASC 350-20)